What is Volatility Trading?

J Pan outlines the importance of implied volatility,

"According to the CFA institute, implied volatility is a measure of the expected risk with regards to the underlying for an option. The measure reflects the market’s view on the likelihood of movements in prices for the underlying, having the tendency to increase when prices decline and thus reflect the riskier picture. Given this predictive nature, implied volatility serves as a useful tool in gauging the overall market condition and provides guidance for trading.

"According to the CFA institute, implied volatility is a measure of the expected risk with regards to the underlying for an option. The measure reflects the market’s view on the likelihood of movements in prices for the underlying, having the tendency to increase when prices decline and thus reflect the riskier picture. Given this predictive nature, implied volatility serves as a useful tool in gauging the overall market condition and provides guidance for trading.

As the term ‘implied’ suggests, it is the implicit or expected future likelihood of the volatility we are projecting as compared to historical volatility. This can also make the reading relatively subjective and not 100% accurate all the time. Do note that although implied volatility is measured as a percentage, which typically surges with sharp declines in prices and decreases as prices retrace losses, it is truly directionless.

Implied volatility is commonly used by the market to pre-empt future movements of the underlying. High volatility suggests large price swings, while muted volatility could mean that price fluctuations may be very much contained.

It is also commonly used in the pricing of options, which as we know may become in the money (ITM) with high volatility, should the volatility help prices breach the strike price in the favourable direction. As such, options with high implied volatility tend to come with higher premiums." Read more...

If a particular market offers options upon it, volatility trading is another manner in which a view of the market can be expressed. As such, the investor is not taking a view of the direction of the market, but its momentum.

The greater the volatility of a market the higher the premium will be, as the probability of any option expiring profitably is greater. In essence it is increased uncertainty in a climate of volatile movement that causes options to be valued at a higher premium.

In order to eliminate the directional risk of the option, the investor needs to hedge the option in the underlying market. So, if it is a call option that is bought, the underlying must be sold. If it is a put option that is bought, the underlying must be bought. The opposite is required if these options are sold.

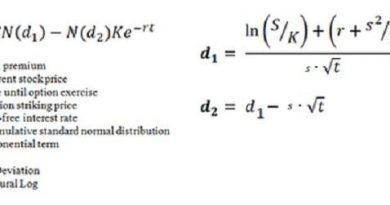

The ratio of options bought or sold, with respect to the number of underlying contracts used to hedge, is known as the Delta. The Delta refers to an options probability of falling in profit on expiry. It is a percentage that, along with numerous other mathematical indicators, is provided expressly by the Black & Scholes mathematical model. In simple terms it represents the probability that the option will expire in profit as analyzed on any given day, using the current underlying market position, days to expiry, the strike price, and the implied volatility used.

An option which is 'at the money' or at the current market position may go either way, and so has a delta of 50%. A call option that is far higher than the market, may have a delta of only 10%, but a put option that is far higher than the market, and so already destined to expire in profit, may have a delta or probability of expiring profitably, of 80%.

So if 10 options that have a strike price at the current market position, the delta would be 50% and so only 5 underlying contracts are needed to hedge it.

Now, as the market moves, wherever it moves, the investor needs to 're-hedge' the position, according to the delta at the new market position. An option that had a 50% delta when it was originally traded, with a 50 point move, will now have a delta that is less or maybe more according to the direction the market has moved. If probability of profitable expiry has increased the delta will be more, and if decreased, it will be less.

The investor will find that when having bought options, re-hedging requires selling underlying contracts when the market moves up, and buying contracts when it moves down. The price of the option changes also, but is offset according to the re-hedging which in this case is buying low and selling high - always making a profit. Buying options, is buying volatility and relies on the market being more volatile.

As options decay in value with time, due to their being an expiry date, re-hedging for a profit needs to occur frequently enough to offset this time decay each day.

Conversely, if options are sold, a loss is incurred each time the re-hedging takes place on a market move, and so selling options relies on the market being less volatile. Time decay works in favor of the option seller, and so losses on re-hedging are required to be less than the time decay received each day.

Simply stated, a seller of options still has unlimited liability, and a buyer, liability limited to the premium paid for the option.

With the use of software, an entire portfolio of options can be calculated to a net sum in terms of risk, volatility and delta for re-hedging.

Selling expensive options and buying cheap options, and maintaining re-hedging techniques, will accrue in profit if a mathematical model is used to value options to a benchmark value.