White Paper Shows Volatility Risk Premium Facilitated Higher Risk-Adjusted Returns for PUT Index

Using more than 32 years of analysis, University of Illinois at Chicago Professor Oleg Bondarenko explored if certain strategies could exploit the richness in pricing of index options. He shared his findings in the recent white paper, “Historical Performance of Put-Writing Strategies” and discussed his research at the 35th annual Cboe Risk Management Conference. See what he has to say below.

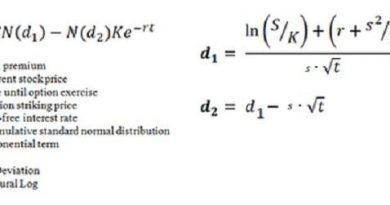

Volatility Risk Premium (VRP) for S&P 500 Options

In his research, Bondarenko found that the S&P 500 Index implied volatility has considerably exceeded its realized volatility. From 1990 to 2018, the average implied volatility, as measured by the Cboe Volatility Index® (VIX®), was 19.3%, while the average realized volatility of the S&P 500® Index was 15.1%. The Volatility Risk Premium (VRP) was a significant difference of 4.2 percentage points.

In light of the existence of the VRP, option-selling strategies may have had the potential to deliver superior risk-adjusted returns when compared to traditional asset classes and option-buying strategies.

Higher Risk-Adjusted Returns for PUT Index since Mid-1986

Professor Bondarenko’s paper analyzed the performance over more than 32 years (from June 30, 1986 to Dec. 31, 2018) of six benchmark indexes: the S&P 500, Russell 2000, MSCI World, Treasury bond and two benchmark indexes that engage in monthly transactions in SPX options.